.svg)

.svg)

.svg)

.avif)

.avif)

.svg)

.svg)

The Queue: Where AI’s Grid Constraint Gets Real

This week’s MacroMashup deep dive examines one of the least discussed datasets in macro markets: The US interconnection queue. More than 2,300 gigawatts of power generation are currently waiting to connect to the grid.

MacroMashup Research Summary

Core Thesis

Markets are obsessed with AI chips.

But the real constraint may be electricity.

The US interconnection queue has become the chokepoint of American electricity expansion. Roughly 2,300 gigawatts of generation capacity are currently waiting to connect to a grid that operates at about 1,200 gigawatts today.

Why It Matters

AI infrastructure, electrification, and energy transition all depend on grid access. Interconnection delays now stretch three to six years in several regions, creating the first major bottleneck in the next wave of electricity demand.

Key Data

• 2,300 GW waiting in US interconnection queues. These projects include solar, wind, battery storage, natural gas, and other generation technologies.

• Only ~13% of projects entering the queue ultimately complete

• Median wait times approaching five years in several regions

• Demand pressure ratios exceeding 5× in ERCOT

Market Signals

The queue is becoming a leading indicator for:

• electricity price pressure

• utility capex cycles

• natural gas demand

• regional AI infrastructure migration

AI models scale at software speed.

Electricity infrastructure expands at infrastructure speed.

The Signal

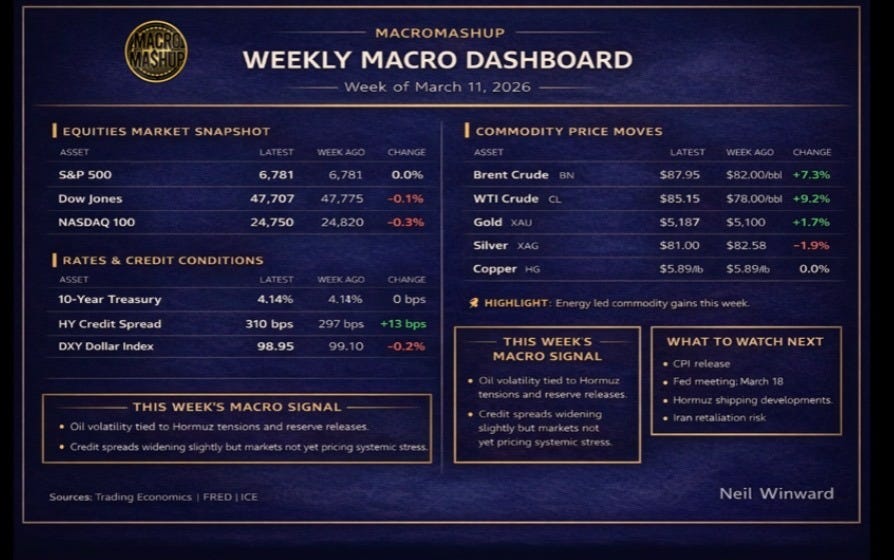

This Week’s Dashboard

It’s all about the barrel.

Oil dominated nearly every signal this week. Brent crude rallied from roughly $82 to $88, while WTI followed closely, settling near $85. The Strait of Hormuz remains the transmission mechanism: tanker transits have collapsed from roughly 24 per day to single digits since the conflict began, and every headline about the Strait is now moving assets across the macro dashboard.

Gold was caught in the crossfire. When oil spikes, the dollar typically strengthens on safe-haven flows and higher yields raise the opportunity cost of holding non-yielding assets. Gold sold off from its late-February highs before stabilizing this week as the dollar softened again. Central bank buying remains the structural floor, but in the short term the dollar and the 10-year yield are driving the tape.

The information war intensified as well. President Trump posted that the conflict was “very complete, pretty much.” Netanyahu responded with a new wave of strikes on Tehran. Iran apologized to the UAE after collateral damage from retaliatory drone strikes — and then continued launching them.

At one point the White House deleted a social media post claiming the US Navy had escorted a tanker through the Strait of Hormuz after confirming no such escort had occurred. Oil briefly dropped on the headline before rebounding.

Meanwhile the IEA proposed the largest strategic petroleum reserve release in its history. Pipeline alternatives are suddenly receiving attention, and the market is attempting to price the difference between a four-week war and a four-month one — a distinction worth tens of dollars per barrel.

Equities barely reacted. The S&P finished the week essentially flat at ~6,781. Credit spreads widened modestly but remain far from pricing sustained economic damage.

Either the market is right.

Or it hasn’t caught up yet.

But the most important constraint shaping the next phase of this cycle may not be geopolitical.

It may be structural.

Because the next phase of the global economy will run on electricity.

The Real Constraint Behind the AI Boom

Last week we introduced the idea that AI’s real constraint may not be software.

It may be electricity.

This intersection between AI infrastructure and electricity systems is becoming one of the most important macro stories of the next decade.

are launching AI Grid Report, a new research publication focused on the intersection of AI infrastructure, electricity systems, and energy markets.

The first issues will examine how the global AI buildout could reshape electricity demand, natural gas markets, and power infrastructure investment.

If you’re interested in how the power grid may shape the next phase of the AI economy, you can preview the project here:

https://open.substack.com/pub/theaigridreport

The first issues will be launching soon.