Oops! Something went wrong while submitting the form.

MacroMashup Research Summary

Core Thesis

Markets are obsessed with AI chips.

But the real constraint may be electricity.

The US interconnection queue has become the chokepoint of American electricity expansion. Roughly 2,300 gigawatts of generation capacity are currently waiting to connect to a grid that operates at about 1,200 gigawatts today.

Why It Matters

AI infrastructure, electrification, and energy transition all depend on grid access. Interconnection delays now stretch three to six years in several regions, creating the first major bottleneck in the next wave of electricity demand.

Key Data

• 2,300 GW waiting in US interconnection queues. These projects include solar, wind, battery storage, natural gas, and other generation technologies.

• Only ~13% of projects entering the queue ultimately complete

• Median wait times approaching five years in several regions

• Demand pressure ratios exceeding 5× in ERCOT

Market Signals

The queue is becoming a leading indicator for:

• electricity price pressure

• utility capex cycles

• natural gas demand

• regional AI infrastructure migration

AI models scale at software speed.

Electricity infrastructure expands at infrastructure speed.

The Signal

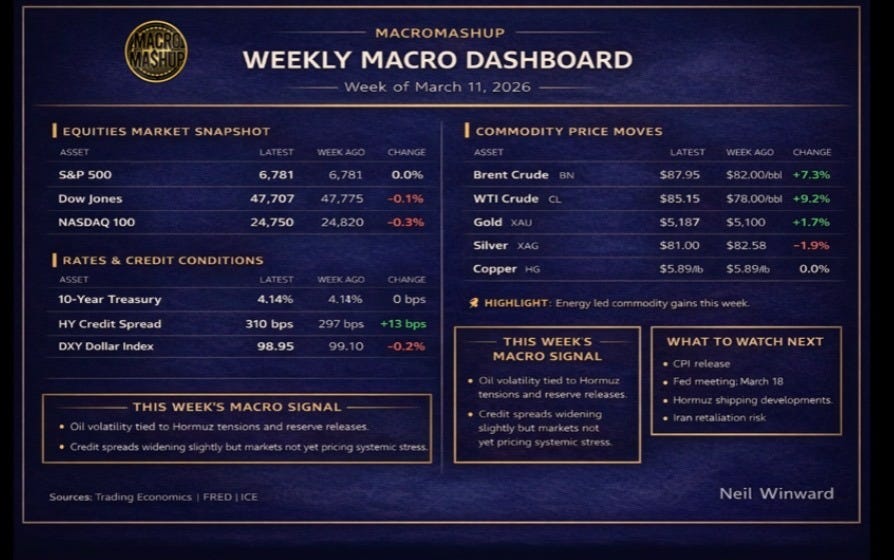

This Week’s Dashboard

It’s all about the barrel.

Oil dominated nearly every signal this week. Brent crude rallied from roughly $82 to $88, while WTI followed closely, settling near $85. The Strait of Hormuz remains the transmission mechanism: tanker transits have collapsed from roughly 24 per day to single digits since the conflict began, and every headline about the Strait is now moving assets across the macro dashboard.

Gold was caught in the crossfire. When oil spikes, the dollar typically strengthens on safe-haven flows and higher yields raise the opportunity cost of holding non-yielding assets. Gold sold off from its late-February highs before stabilizing this week as the dollar softened again. Central bank buying remains the structural floor, but in the short term the dollar and the 10-year yield are driving the tape.

The information war intensified as well. President Trump posted that the conflict was “very complete, pretty much.” Netanyahu responded with a new wave of strikes on Tehran. Iran apologized to the UAE after collateral damage from retaliatory drone strikes — and then continued launching them.

At one point the White House deleted a social media post claiming the US Navy had escorted a tanker through the Strait of Hormuz after confirming no such escort had occurred. Oil briefly dropped on the headline before rebounding.

Meanwhile the IEA proposed the largest strategic petroleum reserve release in its history. Pipeline alternatives are suddenly receiving attention, and the market is attempting to price the difference between a four-week war and a four-month one — a distinction worth tens of dollars per barrel.

Equities barely reacted. The S&P finished the week essentially flat at ~6,781. Credit spreads widened modestly but remain far from pricing sustained economic damage.

Either the market is right.

Or it hasn’t caught up yet.

But the most important constraint shaping the next phase of this cycle may not be geopolitical.

It may be structural.

Because the next phase of the global economy will run on electricity.

The Real Constraint Behind the AI Boom

Last week we introduced the idea that AI’s real constraint may not be software.

It may be electricity.

This intersection between AI infrastructure and electricity systems is becoming one of the most important macro stories of the next decade.

are launching AI Grid Report, a new research publication focused on the intersection of AI infrastructure, electricity systems, and energy markets.

The first issues will examine how the global AI buildout could reshape electricity demand, natural gas markets, and power infrastructure investment.

If you’re interested in how the power grid may shape the next phase of the AI economy, you can preview the project here:

Neil Winward is the founding partner of Dakota Ridge Captial, helping investors, developers, banks, non-profits, and family offices unlock massive tax savings - on average of 7%- 10% - via clean energy investments by fully leveraging U.S. government incentives such the Inflation Reduction Act.

BOOK A CALL

READY TO TAKE ACTION ON YOUR ENERGY PROJECT? BOOK A COMPLIMENTARY, ZERO-OBLIGATION CONSULTATION TO SEE HOW WE CAN HELP YOU.

Markets are modeling AI disruption at software speed. But electricity infrastructure may determine how fast the real economy can absorb it.

Welcome to MacroMashup. We focus on constraints, not forecasts. Market structure, not vibes. Capital flows, leverage, and incentives—where things actually break.

The week’s dominant story is geopolitical.

U.S.–Israeli strikes on Iran. Retaliation spreading across the region. The Strait of Hormuz effectively closed. Markets scrambling to price the energy shock.

But beneath the geopolitical noise, another question is taking shape as Anthropic and OpenAI wrestle with the Department of War over the role AI will play.

The question is not whether AI can transform the economy and the battlefield—it already has— but how fast.

Because AI runs on compute. And compute runs on power.

The constraint shaping the next phase of the AI cycle may not be technological progress.

It may be the infrastructure required to supply electricity fast enough.

In this week’s MacroMashup deep dive, we examine:

• why AI adoption may move at infrastructure speed rather than software speed

• how grid constraints could shape the timeline of economic disruption

• why energy infrastructure may become the leverage point of the AI economy

A look at this week’s dashboard tells the story of which chokepoint is throttling harder.

If you want to understand the structural constraints shaping global markets, join the MacroMashup community.

Subscribe for weekly briefings examining the forces behind the next economic cycle.

The Yen Carry Wobbles, China Steps Back, and Sovereign Duration Stops Feeling Frictionless

Welcome to MacroMashup — where we track the plumbing beneath the headlines.

We focus on funding markets, sovereign balance sheets, and the structural flows that determine which assets become collateral — and which become narratives.

If you’re new here, subscribe for weekly macro breakdowns that connect policy, capital flows, and portfolio positioning — before the consequences become obvious.

Calm Surface, Cracked Foundations

This week’s macro tape looks calm on the surface.

The Fed is in blackout mode, parked at 3.50–3.75%. No new dot plot. No press conference shock. Just a steady drip of inflation and labor data for markets to over-interpret.

There is good and bad in the delayed non-farm payrolls numbers:

Good enough to push back on imminent recession/hard-landing narratives (headline beat, unemployment down, participation up).

Not good enough to erase the story of a materially cooled labor market once you incorporate the 2025 revisions (-900k) and very narrow sector leadership.

For markets: bullish for near-term risk sentiment vs "jobs scare" scenarios, but mildly bearish for front-end duration versus hopes of rapid cuts, with a tilt toward a slow-grind softening rather than a cliff.

January is a volatile month, and not that reliable.

Equities rotate instead of breaking, though the AI scare continues to create anxiety at the white-collar end. The market is beginning to try picking winners and losers.

The 10-year chops around.

Nobody says they’re de-risking — but positioning keeps getting tighter.

Then geopolitics delivers peak 2026 energy: a political standoff over a literal bridge.

The Gordie Howe International Bridge — one of the most important trade crossings between Detroit and Windsor — is now a bargaining chip. The White House is threatening to block its opening unless the U.S. gets a “better deal,” up to and including revisiting permits.

When a concrete span becomes leverage, you’re being reminded of something bigger:

Critical infrastructure is no longer sacred.

It’s collateral.

Under the surface, the real story isn’t about bridges.

It’s about who funds what — and who stops funding it.

In this week’s Deep Dive for paid readers, we examine:

Why the yen carry trade just lost its training wheels

Why Japan’s bond market is no longer “sleepy”

Why China is quietly telling banks to temper Treasury exposure

And what happens when sovereign duration stops feeling frictionless

Bitcoin bled lower this week, behaving less like digital gold and more like a liquidity-sensitive risk asset. Hard assets are beginning to diverge — some are collateral, some are narrative.

Unlock the Opportunities of the Inflation Reduction Act! Are you ready to stay ahead in today's shifting economic landscape? Our comprehensive white paper breaks down the Inflation Reduction Act and reveals the key benefits, incentives, and strategies your business needs to capitalize on. Learn how to optimize your financial planning, leverage tax credits, and position your company for sustainable growth.

Pre-order now to get the insights and actionable steps that can give your business a competitive edge.

New Version Release Date: 12/10/2024

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

.svg)

.svg)

.svg)

.avif)

.svg)

.svg)